Rising AI-driven chip costs are squeezing Chinese EV makers, threatening profits amid a fierce price war. Learn how the industry is adapting now.

The global chip shortage that began in the PC and smartphone sectors is now hitting China’s automotive industry hard. As artificial‑intelligence (AI) applications drive explosive demand for high‑performance semiconductors, Chinese car manufacturers are feeling the squeeze on margins that were already thin from a prolonged price war.

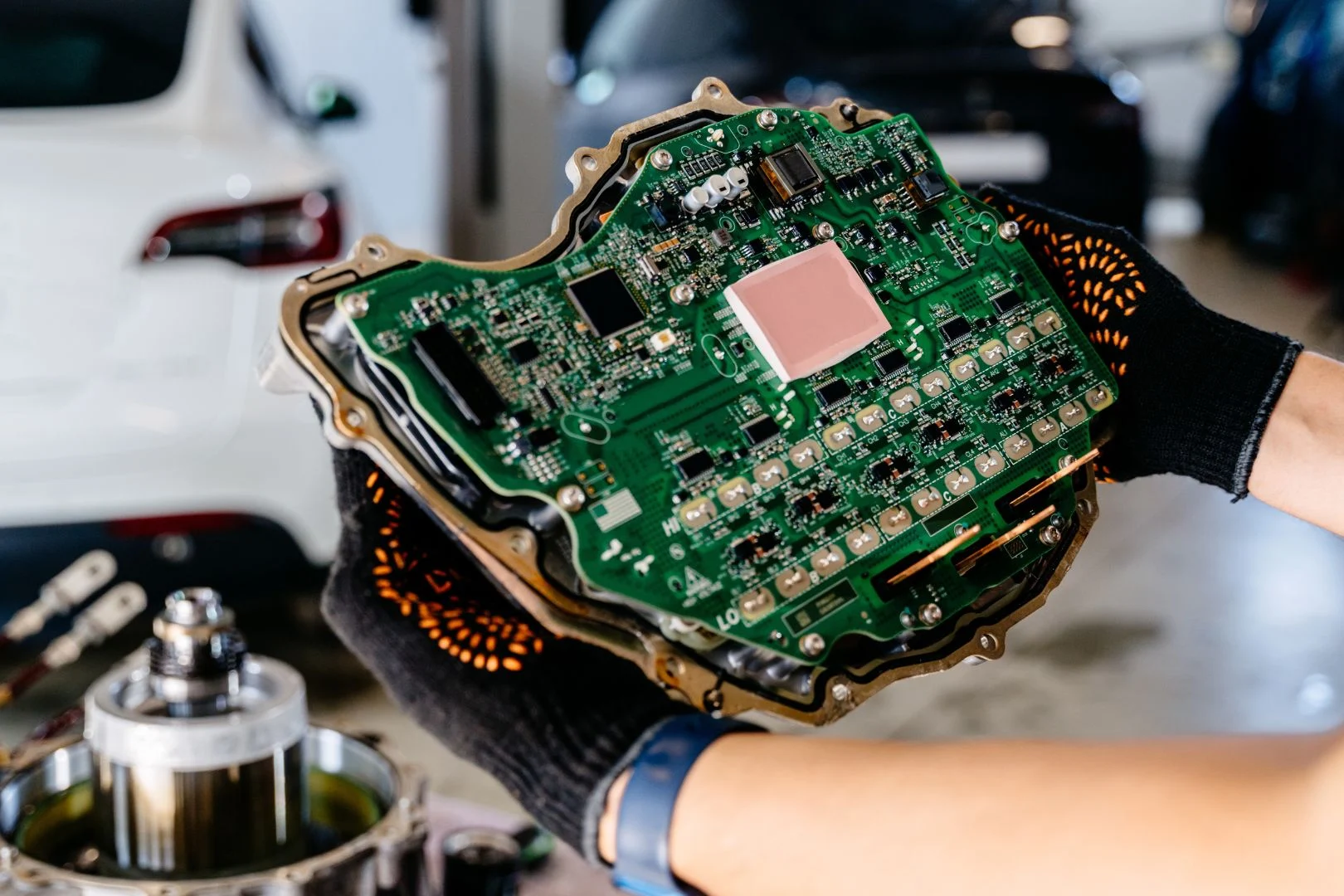

AI Boom Fuels a New Wave of Chip Costs

Semiconductor giants such as Samsung Electronics, SK Hynix and Micron Technology have shifted much of their production capacity to high‑bandwidth memory (HBM) and DDR5 chips used in AI servers. This reallocation leaves legacy automotive chips in short supply and pushes their prices upward.

Analysts predict that the crisis will not ease significantly before the end of 2027, as hyperscale cloud providers continue to pour hundreds of billions of dollars into AI data centres, further hogging the limited supply of specialised chips.

Impact on Leading Chinese EV Brands

Xpeng founder He Xiaopeng admitted that the cost surge for components, especially chips, made pricing the new Xpeng GX SUV “particularly challenging.” He noted that without the recent material price hike, the model could have enjoyed a healthy profit margin.

Similarly, Xiaomi’s CEO Lei Jun apologized to customers of the upgraded YU7 electric SUV, citing “unprecedented chip price increases” as the reason the company could not offer lower prices or more attractive zero‑interest financing.

These statements underscore a broader reality: chips are the nervous system of today’s “software‑defined” vehicles, enabling voice‑controlled cabins, real‑time sensor processing for autonomous driving, and a suite of connected services.

Price Adjustments Across the Industry

In response to rising component costs, several manufacturers have begun to raise prices. Last month BYD lifted the price of its mid‑range driver‑assist package by 21% (about $1,770) citing “global hardware cost increases.”

State‑owned Changan followed suit, adding roughly $440 to the price of its Qiyuan Q07 model equipped with LiDAR, directly attributing the hike to “a sudden surge in global chip prices.”

According to data from the China Association of Automobile Manufacturers, the average selling price of passenger cars in April 2026 rose 2% year‑on‑year to ¥171,000 ($25,200). Yet, even with these adjustments, profit per vehicle fell 13.2% in Q1 2026, dropping to about ¥11,000 ($1,620) per car.

What Lies Ahead for the Chinese Auto Market?

Industry commentator Zhang Yi of iiMedia warns that the ongoing EV price war in China will not end simply because input costs are climbing. When sector‑wide margins stay under pressure, manufacturers are likely to become more cautious about large‑scale discounting and may scale back purchase incentives.

Traditional internal‑combustion‑engine brands, which still rely heavily on price competition to protect market share, will continue to feel the heat, especially in the mass‑market segment around ¥100,000 ($14,700). However, Zhang expects the intensity of price battles to moderate as automakers shift focus toward intelligent driving technology, performance, build quality, safety, and after‑sales service.

In short, while rising chip prices are tightening the profit belt for Chinese car makers, the industry is beginning to pivot from a pure price‑competition mindset to one that emphasizes value‑added features and differentiated technology.