South Korean EV battery giants are pivoting to robot batteries as electric‑car demand wanes. Discover the opportunities and risks – read on now.

Amid a sharp decline in electric‑vehicle (EV) sales, South Korean battery powerhouses LG Energy Solution and Samsung SDI are hunting for fresh growth avenues. Their new target? High‑performance batteries for robots, especially humanoid models that promise higher profit margins than the crowded EV market.

EV Battery Makers Face a Slump

Global EV demand has slowed, dragging down revenue for battery suppliers. In the fourth quarter, LG Energy Solution reported an operating loss of 122 billion won (≈ 84.5 million USD) despite receiving a US subsidy of 332.8 billion won. Samsung SDI posted a 299.2 billion‑won loss for the same period, citing weak US EV demand after tax‑incentive cuts under the previous administration.

Why Robot Batteries Matter

Robots—particularly humanoid platforms—require batteries that are lightweight, boast high energy density, and can endure rapid‑charge cycles. These technical demands translate into higher average selling prices compared with conventional EV cells.

LG Energy Solution Leads the Charge

LG is the fastest mover in the emerging robot‑battery segment. The company supplies cylindrical cells to a range of global robot manufacturers, targeting service robots, autonomous mobile units, and compact yet powerful humanoid platforms. LG says it already serves six of the world’s top technology groups and is negotiating specifications and mass‑production roadmaps for the next generation of robots.

LG’s cylindrical technology, proven in electronic devices and power tools, delivers the light‑weight, fast‑charging performance robot makers need. Expanding into robotics also diversifies LG’s customer base beyond automakers, cushioning it against intensifying competition in the EV battery arena.

Samsung SDI Accelerates Partnerships

Samsung SDI is fast‑tracking its own robot‑battery program through a strategic partnership with Hyundai Motor. The two firms signed a memorandum of understanding last year to co‑develop batteries optimised for robots, focusing on output stability, durability, and flexible packaging. Hyundai, which now owns Boston Dynamics, supplies Samsung with a direct pipeline to one of the United States’ leading humanoid‑robot producers.

Analysts Weigh Opportunities and Limits

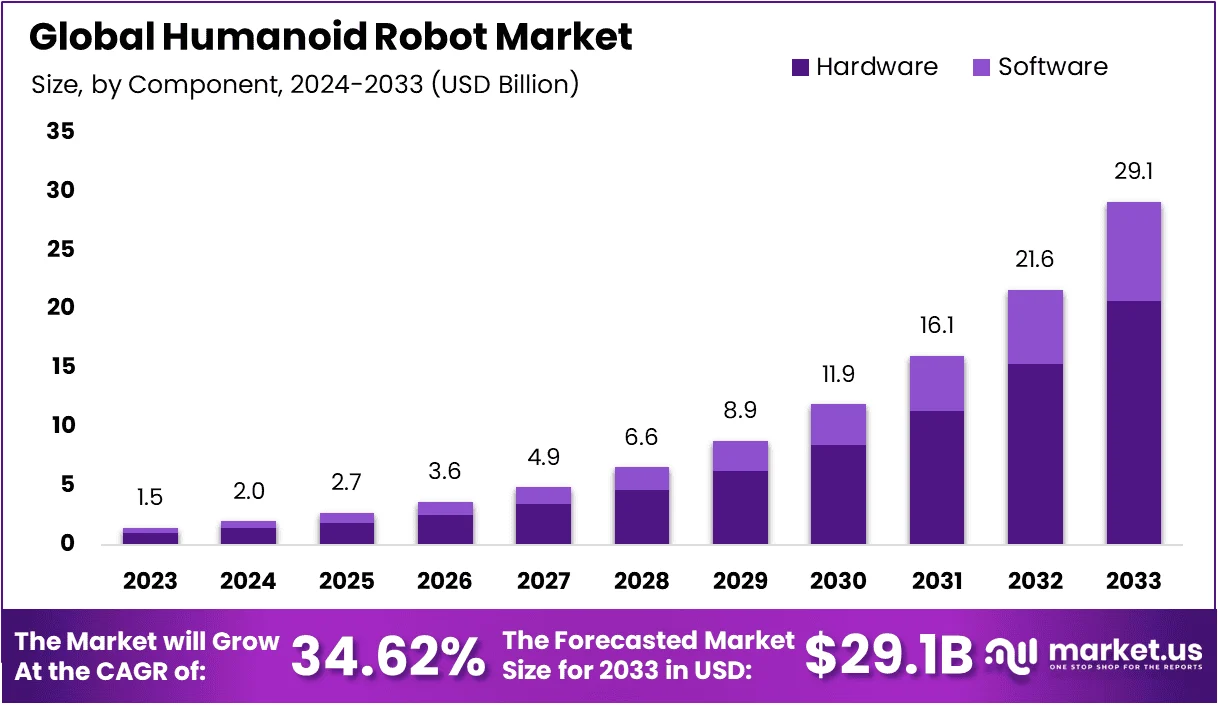

Industry analysts view robotics as a “middle‑ground” market: volumes are modest compared with EVs, but margins are higher and customer relationships deeper. Nomura’s Cindy Park forecasts robot‑battery prices could reach $200‑$350 per kWh by 2030, versus $80‑$120 per kWh for EV batteries.

Long‑term demand is expected to grow in factories, hospitals, hotels, and homes, offering a steadier revenue stream than the boom‑and‑bust cycle that has characterised the EV sector. Still, Nomura estimates the total robot‑battery market will only reach 1‑3 GWh by 2030—far below the 1,647 GWh projected for EV batteries and the 750 GWh for energy‑storage systems.

Hana Securities’ Kim Hyun‑soo cautions that, unlike utility‑scale storage, robot batteries are unlikely to generate a material profit boost for battery makers within the next three years.

Financial Pressures Prompt Diversification

The recent losses have heightened the urgency for Korean battery firms to diversify. While robot batteries present a promising niche, they are not a quick fix for the earnings slump caused by reduced EV incentives in the United States.

Outlook

Expanding into robot power sources is a strategic move that could broaden the customer base for LG Energy Solution and Samsung SDI. However, the modest market size and longer development timelines mean that robot batteries will complement, rather than replace, the core EV business in the near term.